Introduction

Have you ever been involved in a project that was in a bad shape? By “bad shape” I mean the following two scenarios:

- The project is so late and over the budget, that there is no point in continuing it

- The project was a dumb idea from the inception

Have you ever asked yourself a question:

“Why the heck is the management continuing to support this ignominy?”

These projects have been called “runaway trains” and “black swans”. They destroy reputations and companies. So, why is it so difficult to kill them? And yes, I do understand such concepts as sense of attachment, pride and egotism. But if you are a rational, intelligent individual, don’t you have to realize what exactly is at stake (i.e. your company, your shareholders and their money)?

The Kahneman Phenomenon

Enter Daniel Kahneman, a psychologist who won the 2002 Nobel Prize in Economics. In his article titled “Prospect Theory: An Analysis of Decision under Risk” he and his co-author Amos Tversky described the following exercise, that I encourage you to do as well as I describe it.

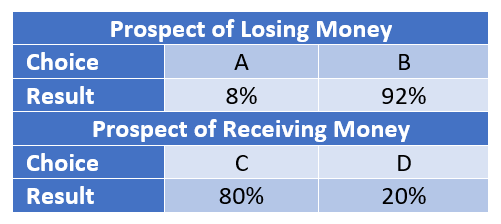

Imagine that I offer you the following two gambles:

Gamble A: A 100% chance of losing $3,000 (i.e. you have $4,000 in your pocket, I threaten you with a gun and walk away with three thousand of your hard-earned money)

Gamble B: An 80% chance of losing $4,000, and a 20% chance of losing nothing (i.e. we throw some kind of dice and there is a 20% that I would leave you alone with your money).

Don’t try to use any statistical or other techniques to answer this question; just go with your gut feel. There is no “right” or “wrong” answer to this question. Which one of these choices would you pick?

Now, let us try a very similar exercise, but instead of robbing you, I am giving you money this time.

Gamble C: A 100% chance of receiving $3000 (i.e. I just give you three thousand dollars)

Gamble D: An 80% chance of receiving $4000, and a 20% chance of receiving nothing (again, we throw dice, and you have a 20% of receiving nothing from me)

What is your choice this time? Again, go with what feels right, rather than trying to assess to choices from the mathematical standpoint.

Scroll down to see Kahneman and Tversky’s findings (see Table 1)

-

-

-

-

-

-

-

-

-

Table 1

The Conclusion

This led them to conclude that when decision problems involve not just possible gains, but also possible losses, people's preferences over negative prospects are more often than not a mirror image of their preferences over positive prospects. Simply put - while they are risk-averse over prospects involving gains, people become risk-loving over prospects involving losses.

When translated into the project management realities this phenomenon perfectly explains the reluctance to kill bad projects, that in essence can be described in the following manner:

If we just throw another couple of thousand (million) dollars at this project, maybe things will turn out to be OK.

The Question

What is your opinion on this matter?

- Kahneman’s explanation sounds about right

- No, I disagree! Executives just don’t know the real picture until it is too late

- No, I disagree! All project can be saved.

- No, I disagree for a different reason (please explain)

About the Author

Jamal Moustafaev, MBA, PMP – president and founder of Thinktank Consulting is an internationally acclaimed expert and speaker in the areas of project/portfolio management, scope definition, process improvement and corporate training. Jamal Moustafaev has done work for private-sector companies and government organizations in Canada, US, Asia, Europe and Middle East. Read Jamal’s Blog @ www.thinktankconsulting.ca

- Please follow me on Twitter:

- Like our page on Facebook:

- Connect with me on LinkedIn:

- Subscribe to my RSS feed:

Jamal is an author of three very popular books:

- Delivering Exceptional Project Results: A Practical Guide to Project Selection, Scoping, Estimation and Management

- Project Scope Management: A Practical Guide to Requirements for Engineering, Product, Construction, IT and Enterprise Projects

- Project Portfolio Management in Theory and Practice: Thirty Case Studies from around the World